Paying your monthly premium offers peace of mind, but a standard homeowners policy is not a magic shield that absorbs every disaster. Discovering a massive gap in your coverage while standing in ankle-deep water or staring at a fallen oak tree turns a stressful situation into a financial nightmare. Many property owners mistakenly assume their policy protects against floods, pest invasions, or the structural decay caused by neglected plumbing. Understanding these eight crucial home insurance exclusions allows you to purchase the right endorsements and perform necessary preventive maintenance before disaster strikes. Let us examine the surprising scenarios your standard policy ignores and learn exactly how to fortify your home, protect high-value assets, and safeguard your landscaping against the unexpected.

Water and Earth: The Uncovered Elements

1. The Reality of Flood Damage Coverage

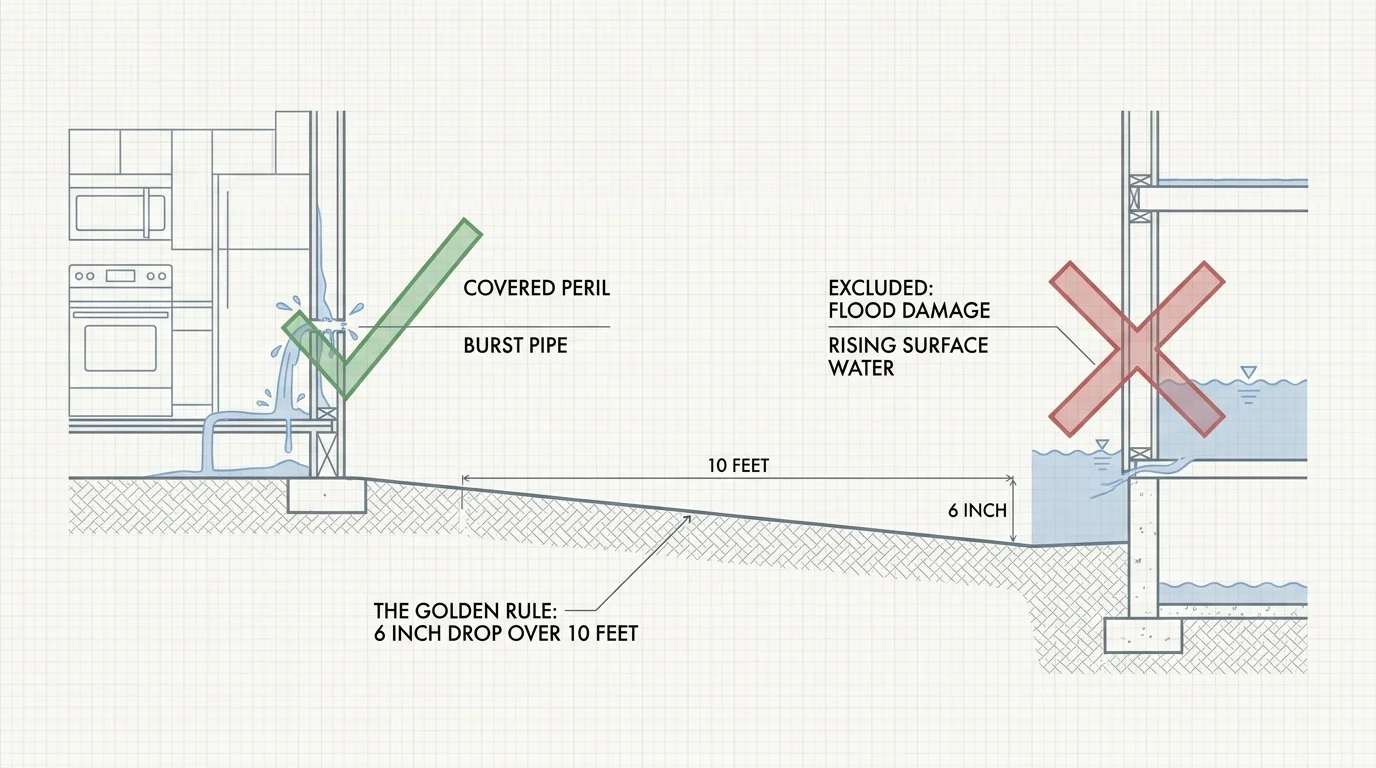

When heavy spring rains overwhelm your garden and send water pouring over your thresholds, your standard home insurance policy will not rescue your ruined hardwood floors or waterlogged drywall. Standard policies strictly exclude flood damage coverage; they define a flood as a rising body of water from the outside moving inland. A burst pipe inside your kitchen wall is typically a covered peril, but storm surges, overflowing rivers, and poor yard drainage that forces groundwater into your basement require a completely separate policy through the National Flood Insurance Program or a private carrier.

Protecting your home from surface water requires active landscape management. Grade your soil so it slopes away from your foundation—a drop of at least six inches over the first ten feet is the golden rule. Install French drains to redirect pooling water in low-lying garden beds, and extend your gutter downspouts well beyond the structural envelope. Proper exterior water management saves your interior walls and preserves the health of your foundational plantings, which easily succumb to root rot in standing water.

2. Earthquakes and Sinkholes

Just as water sweeping across the ground is excluded, the movement of the ground itself falls entirely outside standard coverage parameters. Earthquakes, sinkholes, mudslides, and tremors will ravage brick pathways, collapse retaining walls, and crack foundations—leaving you entirely responsible for the massive repair bills. Property owners living on fault lines or in areas prone to limestone sinkholes must secure specialized earth movement endorsements.

From a landscaping and structural perspective, earth movement heavily impacts how you design your outdoor living spaces. Rigid materials like poured concrete crack violently under stress; flexible paving materials, such as interlocking pavers set on a proper sand and gravel base, ride out minor tremors with far less damage. When designing garden terraces in earthquake-prone regions, utilize reinforced masonry or flexible timber walls rather than dry-stacked stone to prevent sudden collapses during seismic activity.

Gradual Decay: When Time Is the Enemy

3. Maintenance Related Damage and Neglect

Insurance companies exist to cover sudden, accidental disasters—not the slow, creeping deterioration of a neglected property. If a violent windstorm rips off your roof shingles and allows rain to ruin your attic, your policy engages. However, if a slow drip under your indoor plant station rots the floorboards over three years because you failed to fix it, that claim faces immediate denial under the umbrella of maintenance related damage.

Indoor plant enthusiasts must remain particularly vigilant. Heavy ceramic pots placed directly on hardwood floors trap condensation, leading to deep structural rot that insurance adjusters categorize as homeowner neglect. Always elevate your planters using stands or heavy-duty cork mats, and frequently inspect the areas around your indoor humidity tents and water features. Treat your home with careful watchfulness; identifying a slow plumbing leak or a compromised window seal early prevents thousands of dollars in uncovered structural repairs. For thorough checklists on seasonal home upkeep, This Old House offers excellent practical resources.

4. Mold and Fungal Growth

Mold thrives wherever moisture settles, transforming beautiful rooms into hazardous environments. Unless mold results directly and immediately from a covered peril—such as a sudden burst pipe—insurance companies generally exclude mold remediation. Chronic humidity from poor bathroom ventilation, a leaky roof you neglected to patch, or a poorly ventilated indoor jungle room will breed black mold that you must clean up on your own dime.

To prevent localized mold outbreaks, manage the microclimates inside your home. Indoor gardeners utilizing humidifiers for rare tropicals must balance that moisture with adequate airflow. Use oscillating fans to keep the air moving, run dehumidifiers in naturally damp basements, and maintain indoor humidity levels between 40 and 60 percent. Keeping your walls dry and your air circulating protects both your respiratory health and your home’s structural integrity.

Nature Encroaching on Your Living Space

5. Fallen Trees That Miss Your House

A massive, 80-foot silver maple coming down in a severe storm is a terrifying sight. If that tree crashes through your roof, your insurance policy covers the structural repairs and the cost to remove the tree from the house. But what happens if the tree falls across your lawn, crushing your prize-winning rose bushes and ruining your turf, but entirely missing your physical structures? In most cases, you are left holding the bill for the chainsaw crew and the debris removal.

Insurers cover the home, not the yard. Proactive tree care is your best defense. Hire a certified arborist to inspect large trees near your property every few years. They can identify hollow trunks, fungal conks, and heavy deadwood before gravity and wind do the job for them. Regular pruning reduces the wind resistance of the canopy, greatly lowering the risk of an entire tree uprooting during a gale.

“A garden is a grand teacher. It teaches patience and careful watchfulness; it teaches industry and thrift.” — Gertrude Jekyll

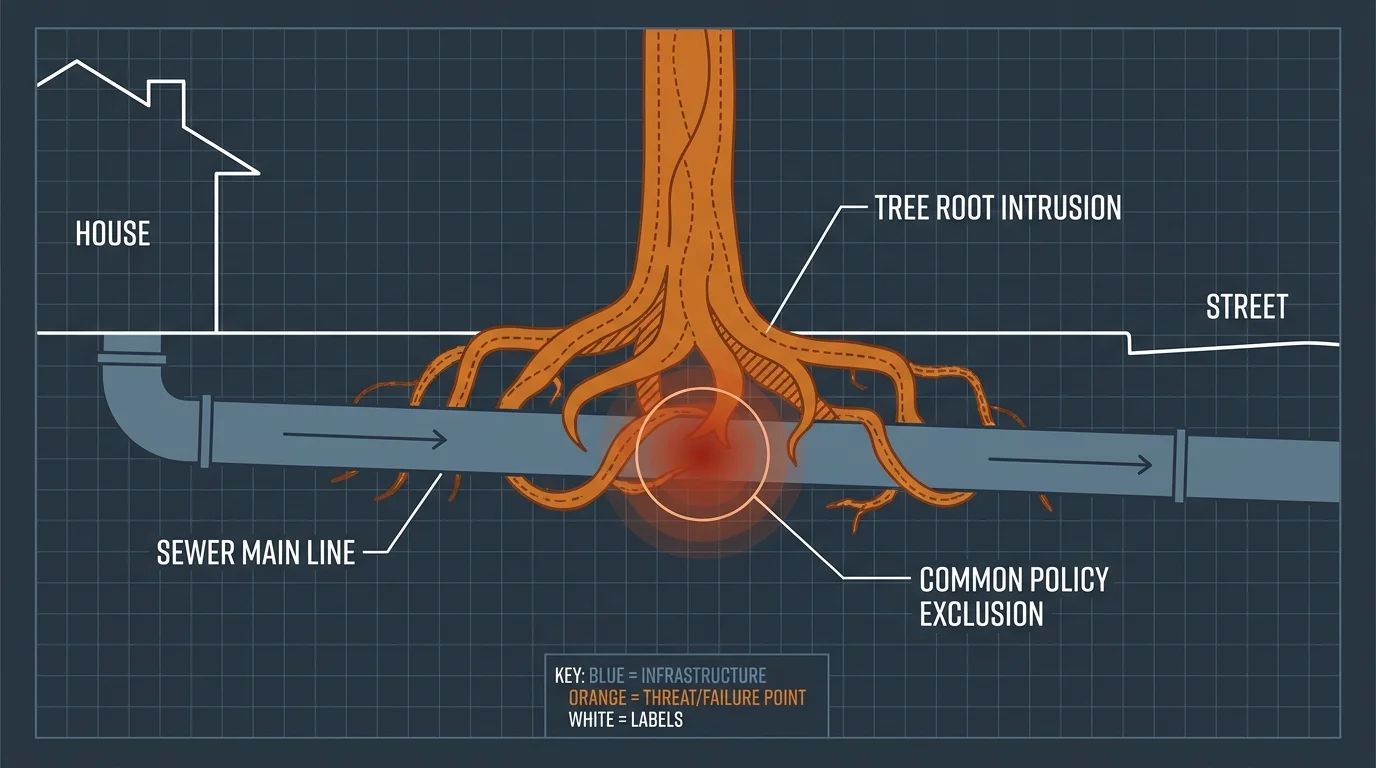

6. Root Intrusions and Sewer Backups

Sewer backups push raw sewage into your home, ruining floors, drywall, and furniture. Surprisingly, standard policies rarely cover sewer and drain backups unless you specifically purchase a water backup endorsement. One of the primary causes of these backups? Tree roots.

Roots possess an incredible ability to sense moisture and nutrients, and they will relentlessly exploit microscopic cracks in aging terracotta or cast-iron sewer lines. Once inside, they proliferate into massive clogs that send wastewater surging back into your basement. Understanding which trees to plant near utility lines is a critical homeowner skill. For detailed guidance on proper tree placement, consult the PennState Extension resources on residential landscaping.

| Tree Species | Root Aggressiveness | Recommended Planting Distance from Pipes/Foundation |

|---|---|---|

| Weeping Willow | Extremely High; highly invasive water-seekers | At least 50 feet away |

| Silver Maple | High; fast-growing surface roots | At least 30 feet away |

| Japanese Maple | Low; compact, non-invasive roots | 10 feet away (generally safe for garden beds near structures) |

| Dogwood | Low; shallow but well-behaved roots | 10-15 feet away |

| Poplar / Cottonwood | Extremely High; destructive to masonry and pipes | At least 40 feet away |

The Fine Print on Your Valuables and Pests

7. Limits on High Value Item Protection

You probably know that an expensive engagement ring or a rare piece of artwork requires a separate schedule or rider on your insurance policy. But what about high-value landscaping or an expensive rare plant collection? Standard homeowners insurance places strict caps on landscaping replacement—often limiting coverage to about $500 per tree or shrub, up to a maximum of 5% of your total dwelling coverage. If a vehicle crashes into your custom-designed Japanese garden and destroys $20,000 worth of mature, specialized specimens, your standard policy will fall drastically short.

Furthermore, indoor houseplant collections are generally considered personal property. While a fire might trigger coverage for your belongings, the payout for your prized Variegated Monstera Albo or rare anthuriums will be minimal unless you have documented their value and discussed high value item protection with your agent. Maintain an updated inventory with photographs and receipts of your most valuable botanical and home assets.

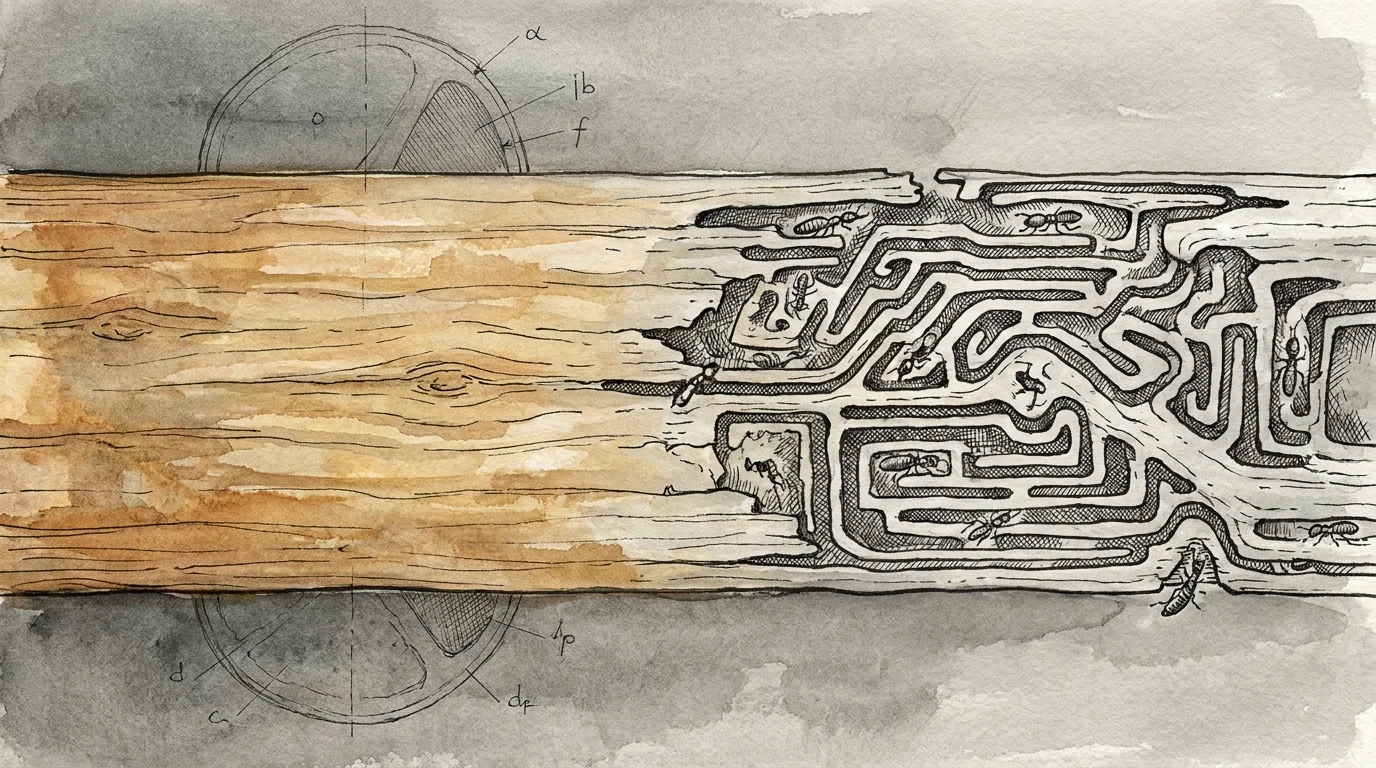

8. Termites, Rodents, and Pest Invasions

Discovering termites chewing through your floor joists or squirrels turning your attic insulation into a maternity ward is a highly destructive scenario. However, insurance companies classify pest control and pest-related damage as preventable maintenance issues. You cannot file a claim to replace the structural beams hollowed out by carpenter ants.

Pest prevention bridges the gap between home maintenance and landscaping. Keep mulch, firewood, and dense shrubbery at least 18 inches away from your home’s siding. Wood-to-soil contact acts as a superhighway for termites. When designing raised garden beds, never build them directly against the side of your house; the constant moisture and organic matter attract insects right to your foundation. For safe, effective pest deterrents, look for products certified by the EPA Safer Choice program.

DIY vs. Hiring a Pro: Preventive Home Maintenance

Keeping your home in a condition that prevents denied insurance claims requires a mix of weekend elbow grease and professional expertise. Knowing when to put down the toolbelt and pick up the phone saves you from exacerbating hidden problems.

- DIY: Managing Surface Water and Gutters. You can absolutely clean your gutters twice a year, attach downspout extensions, and apply fresh caulk to window frames. Monitoring your indoor plant setups for leaks and installing moisture-resistant mats under large pots are simple, effective weekend tasks.

- DIY: Minor Pest Deterrence. Trimming back branches that touch your roof line to prevent rodent access and sealing small foundation cracks with specialized masonry caulk are excellent DIY projects for the proactive homeowner.

- Hiring a Pro: Tree Canopy Management. Never attempt to cut large, overhanging branches near power lines or directly above your roof. A certified arborist carries the proper liability insurance and equipment to drop heavy limbs safely.

- Hiring a Pro: Plumbing Scopes and Grading. If you notice a sudden drop in water pressure or suspect tree roots are invading your sewer line, hire a plumber to run a camera down the pipes. Correcting severe negative grading near a foundation often requires a professional landscaper with a skid-steer loader.

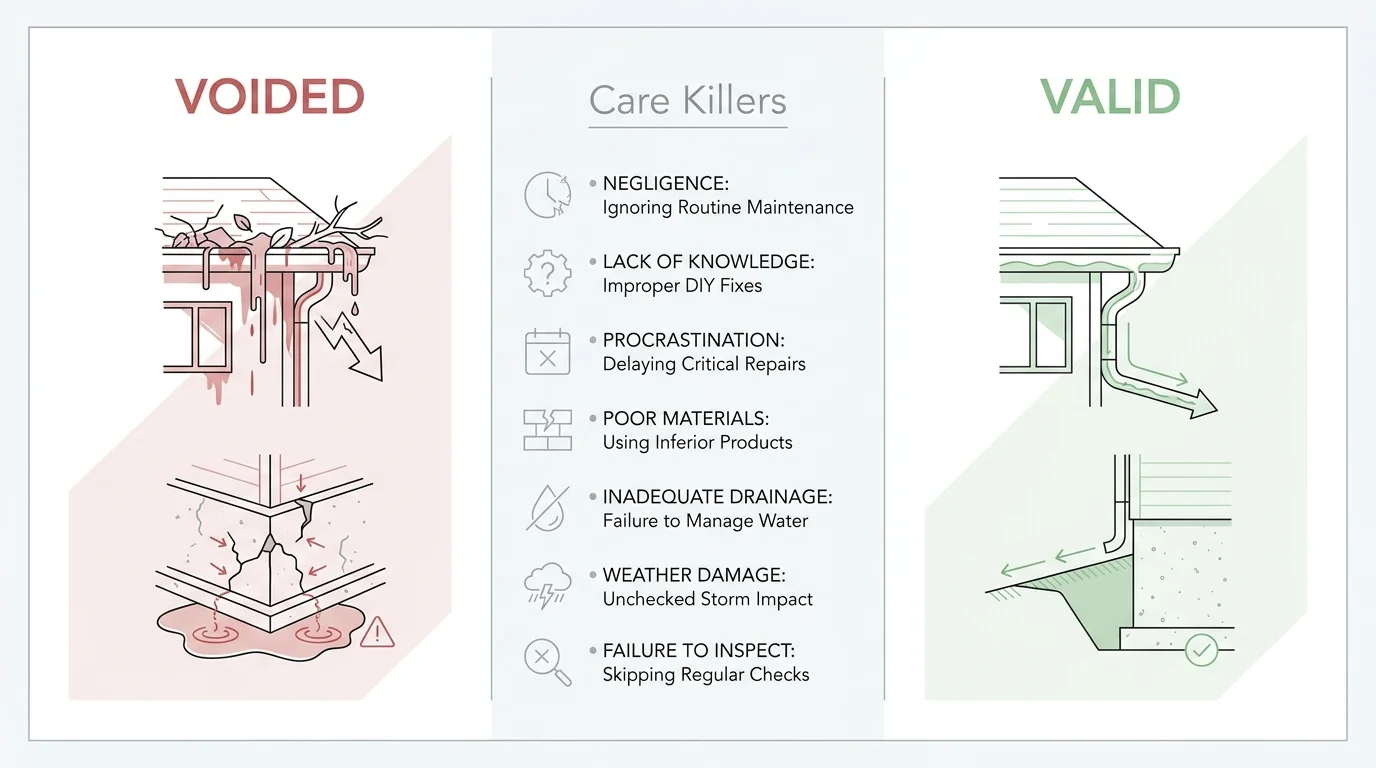

Care Killers: Insurance Voiding Mistakes

Your actions—or lack thereof—can actively void parts of your coverage. Avoid these massive pitfalls to ensure your policy protects you when you need it most:

- Leaving a house vacant without winterizing: If you travel for the winter and leave your home unheated, your pipes will freeze and burst. Insurers universally deny claims for burst pipes in vacant homes where the owner failed to maintain heat or shut off the water supply.

- Ignoring a known leak: Taping a bucket under a leaking pipe for months rather than fixing it guarantees a claim denial when the ceiling eventually caves in.

- Failing to update your policy after a major renovation: If you build a $50,000 sunroom for your plant collection and fail to increase your dwelling coverage, you will be severely underinsured during a total loss event.

- Running a business without notification: Selling thousands of dollars of rare plant cuttings out of your home greenhouse without a commercial endorsement can void your personal property coverage if a fire starts due to your commercial grow lights.

Frequently Asked Questions

Does my policy cover my expensive rare plant collection?

Standard personal property coverage applies to houseplants, but only up to standard limits and only for covered perils (like a fire). If your plants die from a disease, pest infestation, or power outage that cuts off their grow lights, insurance will not cover the loss. For highly valuable botanical collections, you need to discuss specific scheduling or business endorsements with your agent.

Is my landscaping covered if a storm destroys my garden?

Yes, but with strict limitations. Standard policies typically cover damage to trees, shrubs, and plants caused by fire, lightning, explosion, or vehicles not owned by the resident. However, damage caused by wind or heavy snow is usually excluded for landscaping. Furthermore, payouts are usually capped at around $500 per plant.

How do I know if I need flood insurance?

If water pools in your yard during heavy rains, if you live near a body of water, or if your region experiences rapid spring snowmelt, you are at risk. Review the FEMA flood maps for your specific address, but remember that a significant percentage of flood claims come from outside high-risk zones. When in doubt, request a quote; flood insurance in moderate-risk areas is often surprisingly affordable.

Fortifying your home against disaster involves much more than simply paying an insurance premium. It demands active engagement with your property—from grading your soil and pruning your trees to meticulously monitoring your indoor humidity and plumbing. Take time this weekend to walk the perimeter of your home; check your gutters, inspect your foundation plantings, and verify that large trees are healthy and clear of the roofline. By pairing smart preventative maintenance with a thorough understanding of your policy’s limits, you create a living space that is beautiful, resilient, and truly secure. Plant care requirements vary by climate, soil, and growing conditions. Always confirm plant toxicity with your veterinarian using the ASPCA database if you have pets or young children.

Last updated: May 2026. Plant care guidance reflects current horticultural best practices—always observe your specific plant’s signals.